Finance

Compounding Can Add Fuel to Your Portfolio

If you enter the terms "Albert Einstein" and "compounding" into an Internet search engine, you'll discover a wide variety of quotes attributed to the great inventor. Some results say Einstein called compounding the "greatest mathematical discovery of all time," while others say he called it the "most powerful force in the universe." Despite the many variations, Einstein's point is valid: compounding can add fuel to your portfolio's growth. The key is to allow enough time to let it go to work.

Time and money can work together

The premise behind compounding is fairly simple. If an investment's earnings are reinvested back into a portfolio, those earnings may themselves earn returns. Then those returns earn returns, and so on. For instance, say you invest $1,000 and earn a return of 6% -- or $60 -- in one year. If you reinvest, combining that $60 with your $1,000 principal, and earn the same 6 percent the following year, your earnings in year two would increase to $63.60. Over time, compounding can snowball and add up.

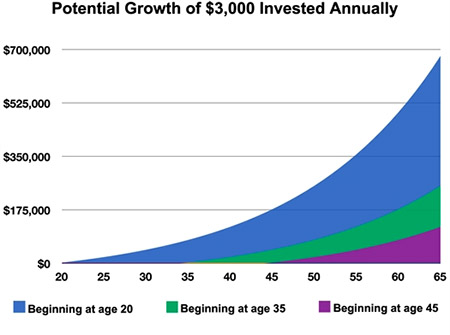

Say at age 45 you begin investing $3,000 annually in an account that earns 6 percent per year, with earnings reinvested. At age 65, your $60,000 principal investment would be worth almost twice as much -- about $117,000. That's not bad, right?

Now consider what happens if you begin investing at age 35, using the same assumptions. By 65, your $90,000 principal would nearly triple to just over $250,000.

Finally, consider the results if you start at age 20: your $135,000 investment would be worth a jaw-dropping five times as much -- $676,524. That's the power of compounding at work.

But how long do I have to wait?

If you'd like to estimate how long it might take for your investment to double, you can use a principle known in investment circles as the "Rule of 72." To use the rule, simply divide 72 by the expected rate of return. For example, if you expect to earn an average of 8 percent over time, the Rule of 72 gauges that your investment would double in approximately nine years. (This rule applies to lump-sum investments, not periodic investment plans such as those given as examples in this article.)

With compounding, the more patience you have, the better off you may be over the long term. The examples in this article assume a steady 6 percent rate of return each year; however, in reality, no investment return can be guaranteed. Your actual earnings will rise and fall with the changing economic and market conditions. That's why it's so important to stay focused on the long term. Over time, the ups and downs may average out, and your earnings can potentially go to work for you.

Perhaps that's why Einstein called compounding "man's greatest invention." Or was it the "eighth wonder of the world"? Regardless ... you get the idea. When it comes to investing, time can be the power behind your potential success.

Bhitti Patel of Capital Insurance & Asset Protection LLC, can be reached at (813) 679-5204, e-mail [email protected] or visit www.mycapitalinsurance.com

Accounting

Mark these tax dates on your 2013 calendar

Don’t subject yourself to tax penalties for missing important filing deadlines in 2013. Get out your 2013 calendar and mark any of the following tax deadlines that apply to you or your business.

- Jan. 15 — Due date for the fourth and final installment of 2012 estimated tax for individuals (unless you file your 2012 return and pay any balance due by Jan. 31).

- Jan. 31 — Employers must furnish 2012 W-2 statements to employees. 1099 information statements must be furnished to payees by payers. (Deadline for providing Forms 1099-B and consolidated statements to customers is Feb. 15.)

- Jan. 31 — Employers must file 2012 federal unemployment tax returns and pay any tax due.

- Feb. 28 — Payers must file information returns (such as 1099s) with the IRS. (April 1 is the deadline if filing electronically.)

- Feb. 28 — Employers must send W-2 copies to the Social Security Administration. (April 1 is the deadline if filing electronically.)

- March 1 — Farmers and fishermen who did not make 2012 estimated tax payments must file 2012 tax returns and pay taxes in full.

- March 15 — 2012 calendar-year corporation income tax returns are due.

- April 15 — Individual federal income tax returns for 2012 are due unless you file for an automatic extension. Taxes owed are due regardless of extension.

- April 15 — 2012 federal partnership returns are due.

- April 15 — 2012 annual gift tax returns are due.

- April 15 — Deadline for making your 2012 IRA and education savings account contributions.

- April 15 — First installment of 2013 individual estimated tax is due.

- June 17 — Second installment of 2013 individual estimated tax is due.

- Sept. 16 — Third installment of 2013 individual estimated tax is due.

- Oct. 15 — Deadline for filing your 2012 individual tax return if you filed for an extension of the April 15 deadline.

ARE YOU REQUIRED TO PAY THE “NANNY TAX” FOR 2012?

A good domestic worker can help take care of your children, assist an elderly parent, or keep your household running smoothly. Unfortunately, domestic workers can also make your tax situation more complicated.

Domestic workers of all types generally fall under the “nanny tax” rules. First, you must determine whether your household helper is an “employee” or an “independent contractor.” If you provide the place and tools for work and you also control how the work is done, your helper is probably an employee. For example, at one end of the spectrum, a live-in housekeeper is probably an employee. At the other end of the spectrum, a once-a-month gardening service may qualify as an independent contractor.

If your household worker is an employee, then you, as the employer, may be required to comply with various payroll tax requirements. For the year 2012, one important threshold amount is $1,800. If you paid your employee this amount or more during the year, you are generally required to pay social security taxes on your worker’s behalf. The 2012 Social Security and Medicare tax for employers is 7.65 percent of your worker’s wages. The employee is responsible for a 5.65 percent tax (4.2 percent Social Security tax plus 1.45 percent Medicare tax) on his or her earnings. This amount could have been withheld from your employee’s wages, or you’re allowed to pay both portions yourself. In addition to Social Security taxes, you may be required to pay federal and state unemployment taxes as well as other state taxes. With these taxes go various deposit and filing requirements, including the requirement that you provide your employee with an annual W-2 form that shows total 2012 wages and withholding by Jan. 31, 2013.

BE AWARE OF HEALTH CARE LAW CHANGES IN 2013

Now that President Obama has been reelected, the 2010 health care legislation he championed is likely to remain the law of the land. Although some provisions have already kicked in and many others are slated for 2014, here’s an overview of the key changes taking effect this year.

Medicare surtaxes. Two new Medicare surtaxes might affect high-income taxpayers. (1) A 3.8 percent surtax applies to the lesser of “net investment income” or the excess above $200,000 of modified “adjusted gross income” (AGI) for single filers and $250,000 for joint filers. (2) A 0.9 percent surtax applies to earned income above $200,000 for single filers and $250,000 for joint filers.

Medical deductions. The “floor” for deducting qualified medical expenses is raised from 7.5 percent of AGI to 10 percent in 2013, but remains at 7.5 percent of AGI through 2016 for those aged 65 or over.

Flexible spending accounts. Previously, there was no limit on contributions to a flexible spending account (FSA) used for health care expenses. Now the limit on contributions to health care FSAs is capped at $2,500.

W-2 reporting. For the first time, W-2s issued in 2013 for wages paid in 2012 must show the benefit employees receive from employer-sponsored health plans. 2012 reporting is optional for employers issuing fewer than 250 W-2s.

Health care tax credit for small businesses. Less than half of the small businesses that qualify are taking advantage of a new tax credit. Under the health care reform law, small businesses may qualify for a tax credit if they pay at least 50 percent of their employee’s health care premiums.

To qualify the business must employ fewer than 25 employees (special treatment for less than full time employees), with average annual wages of less than $50,000.

The maximum credit for tax years 2010 through 2013 is 35 percent of the premiums paid. For 2014, the credit increases to 50 percent.

If you have failed to take the credit in prior years, you can still file an amended tax return and claim the credit.

Kamlesh H. Patel, CPA, can be reached at (813) 949-8889 or e-mail [email protected] or [email protected]

Need More Money? Four Moves to Consider

Regardless of whatever else may await you in life, saving for the future could be one of your biggest financial challenges. That’s why it’s important to take steps now to make sure you’ll have enough money on hand for retirement, family goals or unanticipated financial emergencies.

A common question financial planners hear from clients is, “How can I save more than I’m saving now?” Fortunately, there are several ways you can accomplish that goal with a bit of professional help.

Consider the following:

Monitor expenses. Lowering your expenses by a modest amount such as 1 percent could allow you to boost your savings initiatives as much as a comparable increase in pay.

To gain insights into your current spending habits, consider downloading a budgeting app for your smart phone. They’re much easier to use than they used to be and make expense tracking very simple. For example, many apps allow you to record your income and spending on the go, incorporating information from various accounts, in order to have an up-to-the-minute overview of your financial standing each day. You can then look for inefficiencies – and ways to economize.

Reduce credit card expenses. On average, each US household with credit card debt owes a balance of more than $15,000.1 You can eliminate such debt faster -- and start saving more -- by paying more than the minimum monthly amount on your credit cards each month.

For example, assume you have a $1,000 credit card debt with a 12 percent interest rate. By paying $20 each month, it would take 67 months to eliminate the debt and would cost you $353.43 in interest. But by doubling your monthly payment to $40, you would be out of debt in just 27 months. Your interest costs would be less than half -- $103.28. Then, when you finish paying off your balance, redirect the money you’d been spending on debt each month to a savings or investment account.

Another way to tackle debt expenses aggressively is by consolidating credit card balances to a single, lower-rate card. Comparison shop for the best rates, but beware of “teaser” rates that start low then jump higher after an initial introductory period ends.

Boost contributions. If you participate in a workplace retirement plan, consider increasing your contribution by an additional 1 percent or 2 percent of income. Even if you think that may be too much, try it out for a few months. The extra effort could make a big difference down the road: Contributing even $20 extra each week could provide you with an additional $87,493 after 30 years (before taxes), assuming 6 percent annual investment returns.2

Use windfalls wisely. While it may be tempting to spend a windfall -- such as an inheritance or workplace bonus -- on something fun, it’s probably a better idea to use the money to enhance your long-term financial standing. For example, assuming you invest a $2,000 windfall in an account earning a 6 percent annual rate of return, it could grow to $2,698 after 5 years, $6,620 after 20 years or $12,045 after 30 years (before taxes).2

1Source: CreditCards.com, July 2011.

2These examples are hypothetical and for illustrative purposes only. Your results will vary. Indicated returns cannot be guaranteed. They do not reflect the performance of any actual investment and do not allow for the fees and expenses incurred with investing. Calculations use monthly compounding at an annual rate of 6 percent, however actual investment returns may vary from year to year, which could impact projected values.

Seema Ramroop, financial advisor, Morgan Stanley Smith Barney, can be reached at [email protected] or call (727) 773-4629.